In the winter of the A-share market, securities companies, as key market participants, are enduring hardships alongside stock investors. In an overall bleak industry scenario, different business structures of securities companies mean varying levels of impact. This article analyzes the influence on brokers' revenue from perspectives of reduced IPO quantities and shrinking financing amounts.

Previously, we discussed that securities companies' services include brokerage, investment banking, asset management, proprietary trading, and net interest income. Investment banking (shortened as IB) services are the most specialized, with a strong resource background, mostly dominated by large state-owned brokers.

Despite deep professional and resource barriers, when the macro environment is poor and the stock market continuously weak, with IPO financing obstructed, IB services are hit first.

Brokerage's IB includes securities underwriting and financial advisory revenues. Securities underwriting involves providing financial due diligence and listing guidance to companies planning to go public, with income mainly from underwriting fees of IPOs, linked to the size of funds raised.

If the market is good, with over-raising phenomena, underwriting fees can be substantial.

Financial advisory fees come from acting as consultants for companies intending to merge, offering advice and services in target selection and financial due diligence. In a booming market, companies are optimistic and tend to strengthen through upstream and downstream mergers and acquisitions.

In a downturn, companies become conservative and focus more on cash flow management, affecting financial advisory business. Overall, financial advisory income is minor compared to the significant part of IPO underwriting revenue.

I. Downturn in the market, significant shrinkage in fundraising amounts

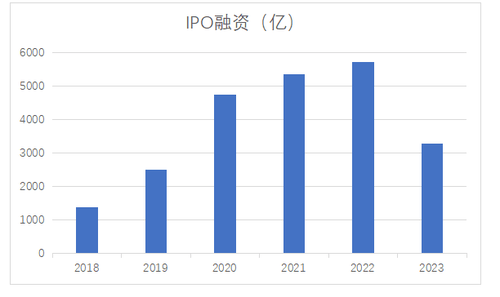

Since 2019, with the pilot registration system in the Science and Technology Innovation Board and the Growth Enterprise Market, there's been an explosive increase in the number of listed companies and the scale of funds raised. Data shows that in 2018, domestic IPO financing amounted to only 137.5 billion yuan, reaching 570.4 billion in 2022, more than triple that of 2018, with continuous growth for four years.

Brokerage IB services and income also saw explosive growth. Taking Citic Securities, the leading domestic brokerage, as an example, its primary underwriting amount for new stocks in 2018 was 12.78 billion yuan, growing to 149.8 billion in 2022, almost tenfold. Securities underwriting income increased from 2.488 billion in 2018 to 5.46 billion in 2022, reaping huge benefits under the registration system.

However, this trend has reversed this year. Affected by the macro environment, this year's Shanghai and Shenzhen stock markets saw a significant reduction in financing amounts, especially since the second half of the year, with the China Securities Regulatory Commission emphasizing balancing investment and financing ends. The investment end aims to attract funds, but this has been minimal, and foreign capital withdrawal has led to reduced incoming funds.

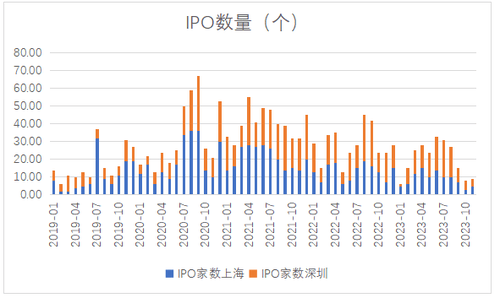

There's been improvement on the financing end, evident from the number of IPOs. In the peak period of 2021, there were more than 50 IPO listings per month. Since 2022, the average number of monthly IPOs has been maintained at 20-30, continuing into the first half of 2023. Starting from last September, the number of IPOs sharply decreased, with only 8 in October and 9 in November, a five-year low.

Looking at financing amounts, the total domestic IPO financing in the first 11 months of 2023 was 328 billion yuan. Considering the recent decrease in meeting numbers and pass rates, the total financing for the year is estimated to be around 350 billion yuan, a 40% contraction compared to last year's 570.4 billion and the first decrease after years of growth.

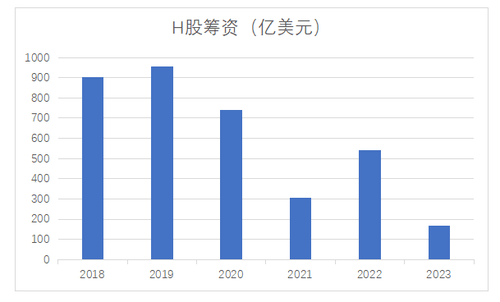

The Hong Kong stock market also saw a contraction. In 2018 and 2019, the financing amounts were 90.2 billion and 95.6 billion USD, respectively. In 2020, it dropped slightly to 73.9 billion due to the pandemic. In 2021, 2022, and the first 11 months of 2023, the amounts were 30.6 billion, 54.2 billion, and 16.8 billion USD, respectively, a significant reduction from the nearly 100 billion USD in previous years. There are jokes online about Hong Kong transforming from an international financial center to the ruins of one.

II. Which companies are most affected?

The sharp decrease in IPO financing mainly impacts brokerages with substantial IB income. As of the first half of 2023, based on securities underwriting income, the top five brokerages are Citic Securities, Citic Construction Investment, Haitong Securities, CICC, and Huatai Securities, ranking with 3.32 billion, 2.425 billion, 1.784 billion, 1.591 billion, and 1.437 billion yuan, respectively. These are known as "Three Citics and One Huatai," along with Haitong.

Extending back to the end of 2022, the top five in underwriting income were Citic Securities, CICC, Citic Construction Investment, Guotai Junan, and Haitong Securities, with Huatai Securities ranking sixth. Generally, these well-established large state-owned enterprises divide the underwriting cake among themselves, with the Three Citics remaining stable, and Haitong, Guotai Junan, and Huatai rotating in the top five.

The contraction in IPO financing impacts these brokerages with substantial IB income, a trend that will continue this year. However, these brokerages are large and have balanced income, with strong resilience.

In conclusion, IPO listing financing has been draining the stock market, likely one reason for its downturn. The reduction in IPOs, in the long run, is good for the market. However, stopping the bleeding isn't enough; the key is to bring in fresh capital."