I. Overall Market Performance

2023 was a year of high expectations and low realities. At the beginning of the year, as the pandemic eased, there was a widespread anticipation that the Chinese economy would rapidly recover similar to the European and American markets. However, due to the drag of real estate and local debt, coupled with the lingering effects of the post-pandemic "scars," the economy experienced a turbulent year with a rapid recovery in the first quarter, lower-than-expected performance in the second quarter, a rebound in the third quarter, and a marginal slowdown in the recovery speed in the fourth quarter.

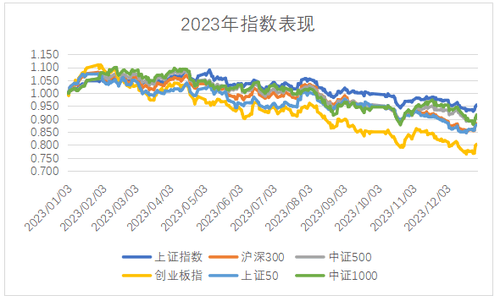

Impacted by factors such as the Federal Reserve's interest rate hikes, economic recovery falling short of expectations, and imperfect stock market systems, the A-share market showed a downward trend throughout the year. Specifically, the Shanghai Composite Index, SSE 50, CSI 300, ChiNext Index, CSI 500, and CSI 1000 had respective changes of -4.54%, -11.93%, -11.75%, -19.74%, -8.84%, and -8.35%. Represented by large-cap stocks, the SSE 50 and CSI 300 indices were weaker due to the influence of reduced holdings by foreign investors, performing less favorably than the CSI 500 and CSI 1000 indices, which represent mid and low-cap stocks, and the ChiNext Index, heavily affected by a substantial pullback in Ningde Times.

II. Individual Stock Performance Ranking

The top ten stocks with the highest gains in 2023 were Kehua Materials, Kunbo Precision, Liant Technology, Shenglong Stock, Jierong Technology, Xici Technology, Gaoxin Development, Haosheng Electronics, Huami New Materials, and Balitaiheng. Among them, six seats were occupied by companies listed on the ChiNext board, making them the biggest winners. The remaining three were from the main board, and one was from the ChiNext board. Do you have any holdings among them?

The top ten stocks with the highest declines for the year were *ST Baolong, *ST Huayi, *ST Zuojiang, Cube Holdings, *ST Aidi, ST Hongda, Yuneng Technology, *ST Fanghai, and *ST Botian. ST Zuojiang, in particular, created a spectacle by hitting the daily limit of a 20-centimeter drop for nine consecutive trading days, resulting in an 84% decline. Among the top ten decliners, seven were ST or *ST stocks, serving as a reminder to be cautious about the decline and delisting risks of underperforming companies.

The total number of delisted companies for the year reached 46, including 44 forced delistings, 1 absorbed through merger, and 1 voluntary delisting. Although the number of delisted companies is still relatively small, the speed of delisting has significantly increased compared to the past. With the improvement of the capital market system, the A-share market is undergoing faster metabolism, creating a favorable environment for value investment.

III. Valuation Levels

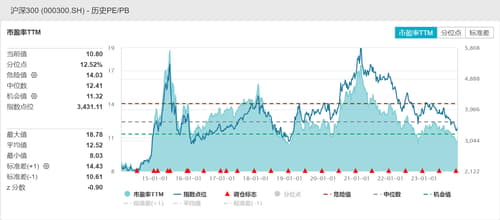

Representing large and medium-sized companies, the valuation of the Shanghai and Shenzhen 300 Index had a trailing twelve-month (TTM) Price-Earnings Ratio (PER) of 10.8 times. The highest value in the past ten years was 18.8 times in 2015, and the lowest was 8.1 times in 2014. The average median for the past ten years was 12.4 times. The upper standard deviation risk value was 14.1 times, and the lower standard deviation risk value was 11.3 times. The current PER of 10.8 times presents a clear undervaluation opportunity.

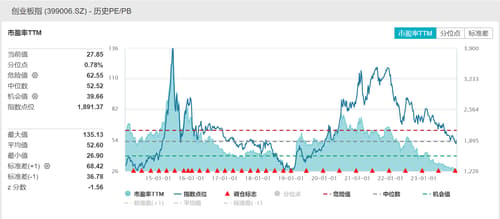

Representing emerging and growth economies, the ChiNext Index had a TTM PER of 27.8 times. The highest value in the past ten years was 135 times in 2015, and the lowest was 28 times at the end of 2018. The average median for the past ten years was 52.5 times. The upper standard deviation risk value was 62.5 times, and the lower standard deviation risk value was 39.6 times. The current PER of 28 times is consistent with the pessimistic expectations at the end of 2018, significantly lower than the normal period, indicating a clear undervaluation opportunity.

IV. Outlook for 2024

Looking ahead to 2024, we are not pessimistic; instead, we are full of expectations for the coming year. The specific reasons include:

- With the Central Economic Work Conference focusing on economic stability and growth in the coming year, issues such as real estate and local debt are expected to be alleviated, paving the way for continued steady economic recovery.

- The peak of the Federal Reserve's interest rate hike cycle is expected, and there is a general belief in the market that there will be 1 to 2 interest rate cuts in the middle of next year. This will result in a reduced suction effect on new capital funds, improved liquidity next year compared to this year, and a better outflow of foreign capital.

- With the comprehensive deepening of the registration system and unprecedented regulatory measures against illegal activities by regulatory authorities, improvements in mechanisms such as reduction of holdings and margin trading will create a favorable environment for the stock market. As China strives to become a financial powerhouse, capital markets will enter a post-value investment era.

- In summary, valuations are at historically low levels, and there is limited downside space for the index. Factors such as the 20th Third Plenary Session, the Federal Reserve's interest rate cut, and the construction of the stock market system may exceed expectations. The capital market in the coming year is worth looking forward to. However, it is important to note that many small and medium-sized companies with inflated valuations may experience long-term bubble bursts and marginalization.