Flowbank has gone bankrupt.

This is the second Swiss bank to go bankrupt after Credit Suisse, Switzerland's second-largest bank.

Global investors are once again questioning the safety and reliability of Swiss banks.

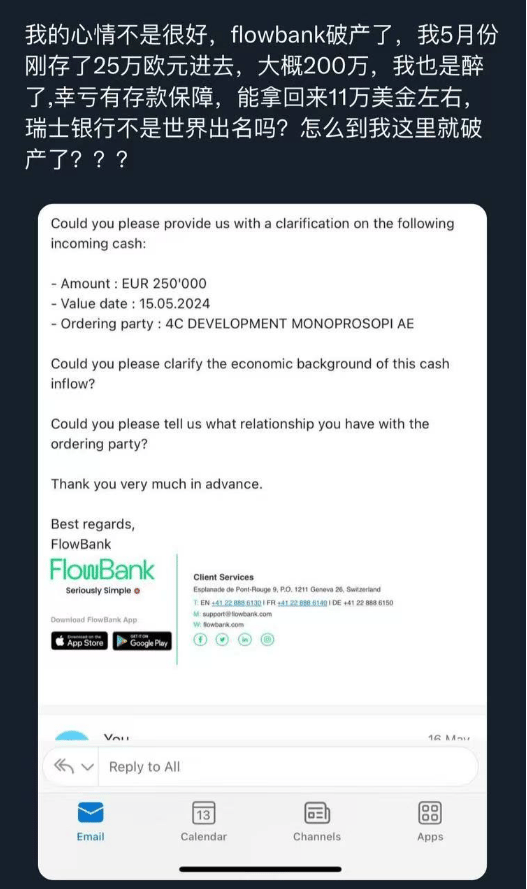

(Image information shared by netizens)

Flowbank Official Announcement

In summary: the bank will close its positions according to relevant clauses and proceed with bankruptcy liquidation as soon as possible.

About Flowbank

FlowBank was established in 2020 as a Swiss online bank providing cryptocurrency services, forex, and CFD contracts.

Headquartered in Geneva with offices in Zurich and Dubai, it is a licensed bank approved by the Swiss Financial Market Supervisory Authority (FINMA) and a member of esisuisse and the Swiss Bankers Association. In the cryptocurrency market, Flowbank is the banking partner of Techteryx, the issuer behind the stablecoin TrueUSD. CoinShares holds part of FlowBank's equity, and FlowBank has previously provided banking services for Binance.

Founder is Former CEO of UK Forex Platform LCG

Flowbank's founder is Charles Henri Sabet, the former CEO of the UK forex platform London Capital Group (LCG).

During his tenure as CEO, the company lost market share to competitors IG Group and CMC Markets, leading to his eventual retirement from the company.

He had also established a Swiss bank named Synthesis Bank in his early career, which was acquired by Denmark's Saxo Bank (currently controlled by Geely Group) in 2007 and gradually evolved into Saxo Bank's Swiss branch, Saxo Bank (Switzerland).

Reasons for Flowbank's Bankruptcy

FINMA stated: the bank lacked sufficient capital to maintain its banking operations and "seriously violated minimum capital requirements." Additionally, there is ample reason to believe that the bank is currently over-indebted with no prospects for restructuring.

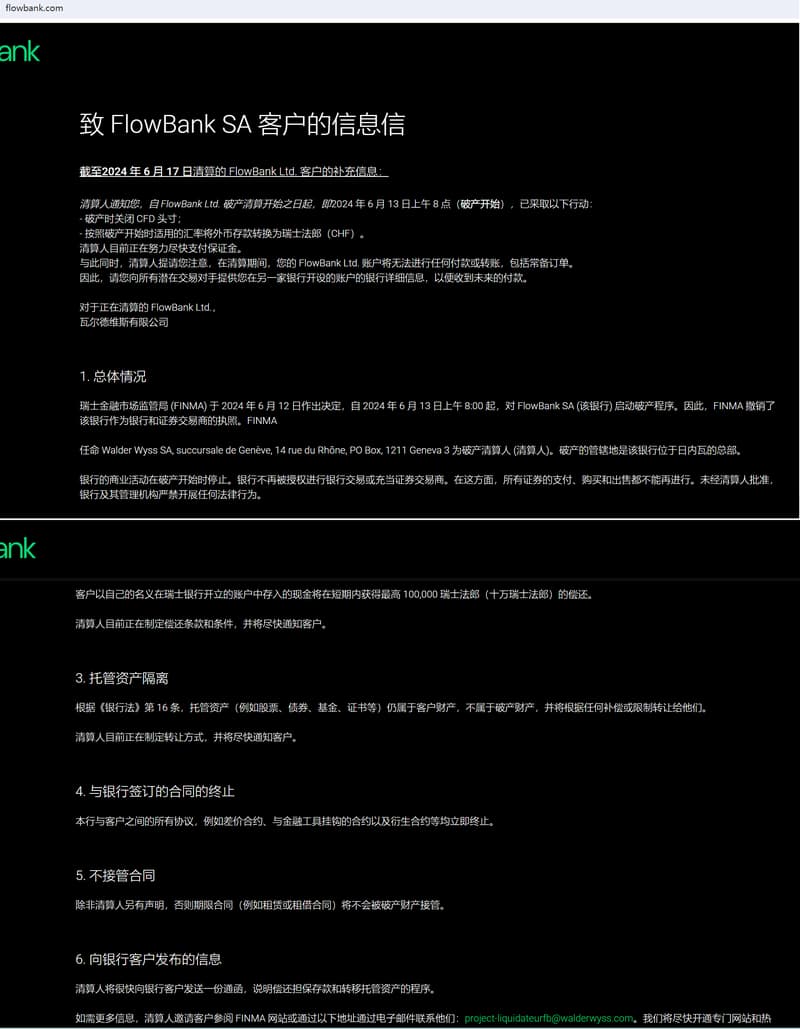

Here is a detailed report by FINMA

(The above is a notice from Swiss regulator FINMA)

Reasons for Flowbank's Bankruptcy:

1) The bank lacked sufficient minimum capital to operate;

2) There is ample reason to believe that the bank is over-indebted;

3) Severe misconduct and long-term non-compliance with license conditions;

4) No possibility of restructuring.

Flowbank's financial reports and audits also had issues with inaccuracies and incompleteness. It established numerous high-risk business relationships and handled a large volume of transactions, increasing the risk; this is one of the reasons leading to its bankruptcy liquidation.

Currently, FINMA has appointed the Swiss law firm Walder Wyss as the bank's bankruptcy liquidator.

Reviewing Flowbank's development, we can see that negative news has been constant since its inception, indicating relatively lax supervision by FINMA.

Founded in 2020, it received the Swiss FINMA banking license in July of the same year.

In October 2021, FINMA discovered serious regulatory violations and took enforcement action.

In October 2022, FINMA ordered extensive measures to regularize the bank and appointed an independent auditor to oversee the implementation.

In June 2023, FINMA again took enforcement action due to ongoing capital ratio violations and deficiencies within the regulatory domain.

On March 8, 2024, due to severe breaches of law and long-term non-compliance with licensing conditions rendering it unable to restore legal effectiveness, the bank's loan application was revoked.

On June 13, 2024, FINMA announced the closure of Flowbank and initiated bankruptcy liquidation.

Flowbank's Customer Compensation:

1) Depositors with amounts below 100,000 Swiss francs will be protected and receive their deposits within seven days.

2) Customers with deposits exceeding 100,000 Swiss francs will be affected by FlowBank's liquidation.

3) It is uncertain whether cryptocurrencies will be classified as custodial assets and thus protected; this will ultimately depend on the liquidator.

Flowbank's bankruptcy is not expected to trigger Switzerland's bank deposit insurance scheme (esisuisse).

esisuisse is a private association with 288 members, including 241 active banks and 40 active brokers, holding deposits of 489 billion Swiss francs as of December 31, 2020.

In 2023, Switzerland's second-largest bank, Credit Suisse, went bankrupt due to regulatory issues, scandals, and poor management, resulting in the evaporation of many depositors' assets and subsequently leading to massive capital outflow.

Economists suggest: The credibility of the Swiss banking system has entirely collapsed.

Although this view is overly harsh, after a series of incidents, the safety that Swiss banks prided themselves on is gradually crumbling in the minds of global investors.

6 Tips for Traders from Flowbank's Bankruptcy:

1) Banks are not absolutely safe and can face bankruptcy risks;

The bankruptcies of Lehman Brothers, Silicon Valley Bank, Credit Suisse, and FlowBank all illustrate this point.

2) Regulation is not absolutely crucial;

Whether in Switzerland, FCA, the United States, or Australia, even strongly regulated platforms still face bankruptcy risks.

3) Insurance offered by platforms is not absolutely secure;

Many brokers offer deposit insurance, which is meaningless for large-scale clients.

4) Custodian banks/methods determine the true safety of customer funds;

The bankruptcy of Silicon Valley Bank shows that smaller banks in major countries are unsafe; Credit Suisse's bankruptcy shows that large banks in small countries are unsafe; FlowBank's bankruptcy shows that small banks in small countries are even less secure. The most reliable are large banks in major countries, like Barclays in the UK, JPMorgan Chase, and Bank of America in the USA.

The method of fund custody is equally important: is it mixed with the broker's own funds? Segregated accounts? Independent segregated accounts? Or PB settlement accounts?

5) Choose brokers with a long operating history and good trading environments;

The longer a platform has been operating, the more stable it tends to be in various aspects. Brokers with just 3 to 5 years of operation should be approached with caution. Trading environments can be evaluated based on execution speed, liquidity, freezing, and slippage.

6) Don't worry too much about leverage or overnight interest; these are secondary considerations to a secure platform.

Leverage of tens of times is usually sufficient, and the real market does have overnight interest; as long as the broker is safe, these factors need not be overly concerned.

That's all for today's sharing,

For more forex-related content, you are welcome to add Lao A on WeChat: TraderLaoa