Market Review

Market Focus

China Market

1. Slowdown in China's August CPI and PPI Decline

Influenced by the continued recovery of the consumer market, ongoing improvement in supply and demand relations, partial improvement in industrial product demand, and the rise in international oil prices, China's national consumer price index (CPI) for August rose by 0.1% year over year, significantly outperforming July's year-over-year decline of 0.3%; the producer price index (PPI) for August increased by 0.2% month over month, compared to a decline of 0.2% in the previous month.

2. Global Prominent Sovereign Funds Declare Unchanged Investments in China

Norges Bank Investment Management (NBIM) announced it has initiated the process of closing its Shanghai representative office due to operational considerations, but its investments in China remain unchanged. NBIM is the operational organization for the Government Pension Fund Global (GPFG) of Norway, one of the world's largest sovereign wealth funds. Data indicates that as of the end of 2022, NBIM had invested in about 850 Chinese companies, with a total value of approximately $42 billion.

3. The Ministry of Housing and Urban-Rural Development States Significant Impact of the "Recognize House But Not Debt" Policy

The transition from recognizing both house and debt to recognizing only the house underscores the alteration in the supply and demand relationship in China's real estate market over 13 years, as well as timely policy adjustments and optimizations. Pu Zhan, Deputy Director of the Policy Research Center of the Ministry of Housing and Urban-Rural Development, noted that surveys suggest the overall national homebuying intention could increase by approximately 15 percentage points, with potentially higher increases in first-tier cities.

Overseas Market

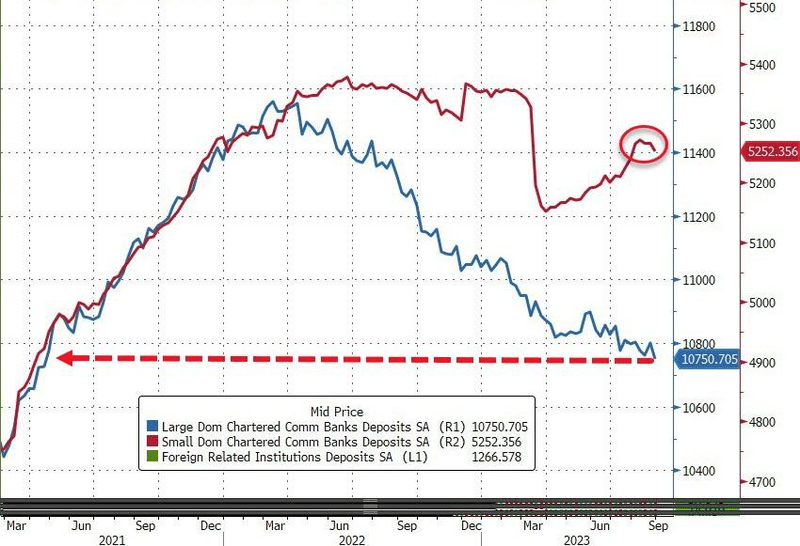

1. American Small Banks Experience Massive Deposit Outflows Again

The crisis of regional banks in the United States has been ongoing for half a year, yet the confidence of investors and depositors in small American banks hasn't been restored. Data shows that large banks saw deposit outflows exceeding $50 billion, the highest level since July, and small banks experienced more than $15 billion in deposits outflow, the largest since March. Additionally, after seasonal adjustment, the total deposit amount in American banks plummeted by $70 billion, dropping to the lowest level since May. Here, large bank deposits reached the lowest level since April 2021, and small bank deposits hit the lowest since July this year (see below).

2. Strike Imminent at the Three Major American Automakers

Shawn Fain, President of the United Automobile Workers (UAW), stated during a Facebook live broadcast that the union rejected the terms of the "Big Three" automakers—General Motors, Ford, and Stellantis North America's parent company, Chrysler. Without further progress, a strike is set to occur next Thursday. The automotive industry, including foreign companies operating in the United States, represents about 3% of the US GDP. Strikes at the three major factories would not only result in substantial losses for the “Big Three” but also impact the American economy for some time to come.

3. Chevron's Australian Natural Gas Facility Prepares for Strike

Following failed mediation talks between the union and Chevron, workers at Chevron's Gorgon and Wheatstone liquefied natural gas (LNG) projects in Australia are set to commence strike action. The union mentioned that a full-scale strike spanning two weeks might occur if ongoing disputes related to salary and working conditions remain unresolved. Australia's Gorgon and Wheatstone supply over 5% of the world's natural gas.

What to Watch Next Week

Next week, investors should pay attention to key data including the Eurozone and Germany's ZEW Economic Sentiment Index, the US August CPI, API and EIA crude oil inventory changes, initial unemployment claims, industrial production, and other economic data. Additionally, investors should keep an eye on the speech by the Bank of England's Chief Economist Huw Pill, the European Central Bank's interest rate decision, and other risk events.