Brokerages Drastically Reduce Commissions, Improving Stock Market Ecology

The year 2023 marks the second year of the bear market for stocks. Into the second half of the year, the index fluctuated at low levels, with the defense of the 3000-point benchmark frequently challenged, and by the end of the year, the defense line was further pushed back to 2900 points. With the market continuously sluggish and trading volumes shrinking, many small and medium-sized brokerages could no longer endure.

The income of brokerage businesses can be categorized into brokerage operations, investment banking, asset management, proprietary investments, etc. For larger brokerages, these lines of business are relatively balanced and do not rely solely on brokerage operations. However, for small and medium-sized brokerages, brokerage operations might be their sole source of income.

Brokerage business income includes commissions from stock and fund transactions, the interest spread from financing and securities lending, and the interest spread on margins. With the exception of the margin interest spread, which demonstrates rigidity and less sensitiveness to market sentiment, the other segments are closely linked to the activity level of the stock market and have been greatly affected by the prolonged downturn.

In addition to the market downturn, the commission reduction initiative promoted by the China Securities Regulatory Commission (CSRC) since the second half of last year has also had a significant impact on the brokerage commission income, making an already challenging brokerage business even more difficult, with this chill persisting into the current year.

I. Stock Market Remains Sluggish with Decreased Trading Volume and Balance of Margin Trading

The stock market in 2023 continued the bear trend of 2022. Throughout the year, the Shanghai Composite Index fell by 4.5%, with the CSI 300 Index, representing large market capitalizations, dropping by 11.75%, and the ChiNext Index, symbolizing the new economic driving force, also performing poorly with an annual decline of nearly 20%. A large number of companies saw their stock prices cut in half, and the number of companies delisted throughout the year reached 46, equal to the sum of the previous ten years, leaving the market lacking a profit effect.

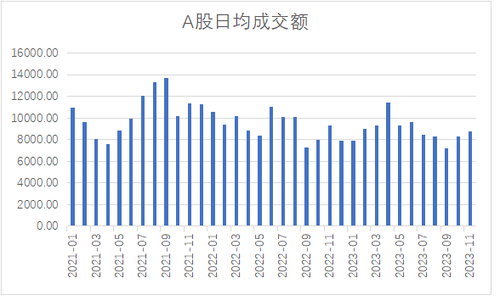

The average daily transaction volume of A-shares shrank dramatically, with the average daily transaction volume falling to 719.7 billion in September, making it the lowest in the past five years. Following comprehensive measures by the CSRC in funding, investment, and trading areas, there was a rebound in volume from October to November. However, the volume shrunk again after December, with the lowest daily transaction volume only reaching 623.3 billion.

Looking at the first 11 months of the year, the average daily transaction volume was 886.1 billion, down by 4.2% compared to 924.5 billion in 2021, and down by 16% compared to the daily average of 10,572 billion in 2021, sliding for two consecutive years.

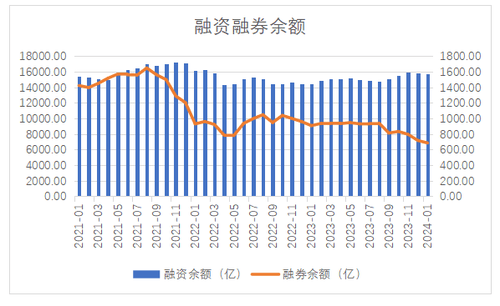

The balance of margin trading, which includes both financing and securities lending, was also affected by the sluggish market sentiment, with the financing business making up the lion's share. As of the end of last year, the financing balance of the Shanghai and Shenzhen stock markets was 1.5741 trillion, while the securities lending balance was only 68.49 billion, a mere fraction of the financing amount.

During times of favourable market conditions with effective profit making, the demand for financing is strong and the financing balance rises, as seen in the obvious profit effect in 2021, when the financing balance of the two markets peaked at 1.72 trillion. However, since 2022, the financing balance has been in continual decline, dropping to 1.58 trillion by year-end, a reduction of over 140 billion from the peak period.

Despite individual investors being the main participants in the financing business, the securities lending business, which primarily serves quantitative strategies and T0 strategies of funds, is likewise affected in an environment of shrinking transaction volume and reduced stock market volatility.

According to Wind data, the securities lending balance in August 2021 was 164.8 billion, whereas at the end of last year it was only 71.6 billion, more than halving from the peak period of 2021.

In addition to the decline in transaction volumes and the financing balance, the reduction of transaction commission rates also took effect in the second half of the previous year.

II. Decrease in Transaction Commission Rates Adds Frost to the Already Chilly Industry

In August last year, the CSRC intensified its efforts to reform the investment side of the capital market, launching the following measures: first, lowering the securities transaction handling fees and, in parallel, reducing the commission rates of securities companies. Second, further expanding the scope of financing and securities lending targets, reducing the rates for financing and securities lending, and including ETFs in the targets for securities lending. Third, refining the regime for reducing shareholdings, enhancing the supervision of illegal reductions and "bypass" reductions, and simultaneously punishing illegal depository activities. Fourth, optimizing transaction supervision to enhance the convenience and fluidity of trading and improving the transparency of trading supervision, with plans to roll out a programmed trading reporting system in due time. Fifth, studying the potential extension of the trading hours in the A-share market and the exchange bond market to better meet the needs of investment and trading.

Subsequently, CITIC Securities took the lead in lowering the trading commission rates for existing investors, followed by announcements from Guotai Junan Securities, Haitong Securities, CITIC Construction Investment Securities, Huaxin Securities, and several other brokerages to reduce trading commissions. However, according to industry insiders, the actual impact of these reductions on commissions is minimal. After nearly 10 years of continuous decline, brokerage commissions have reached an extremely low level and cannot be reduced further.

However, the actual steps to reduce the commission rates for public funds quickly followed. On December 8th last year, the CSRC issued the "Regulations on Strengthening the Management of Securities Trading by Publicly Raised Securities Investment Funds," as a complement to the investment end reform. This "Draft for Comments" stipulated that "the transaction commission rate for passive equity funds shall not exceed the average market transaction commission rate," which will drive down the commission rates for public funds and add snow to the already contracting transaction commissions.

Prior to this, the transaction commission rate paid by public funds to brokerages was around 0.008%, much higher than the average market commission level. The Securities Association of China disclosed that the average single-side stock transaction commission rate, based on net income from security trading by brokerages for the first three quarters of 2022, was about 0.0025%. According to the "Draft for Comments," the public fund transaction commission rate is expected to drop from 0.008% to roughly 0.005%, a reduction of about 30%.

III. Improving the Stock Market Ecology

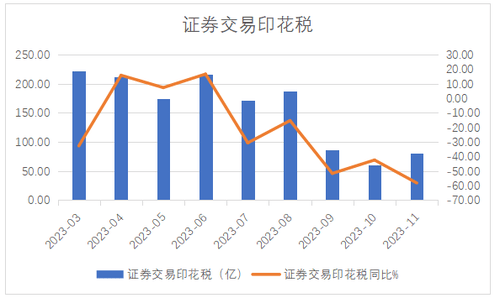

Securities transaction stamp duties are also trending downward. In the first half of the year, the securities transaction stamp tax in the Shenzhen and Shanghai stock markets remained around 20 billion, down from the monthly peak of over 30 billion in 2021. At the end of August, the State Taxation Administration implemented a 50% reduction in the collection of securities transaction stamp tax, resulting in stamp duty being halved in September, with September, October, and November collecting only 8.7 billion, 6.1 billion, and 8.1 billion respectively, less than a normal month's stamp tax.

While it becomes increasingly difficult for brokerage firms to "make easy money," these developments may be beneficial for investors. As discussed earlier, the reduction in IPOs eases the capital drain from the stock market, and the lowering of transaction commissions and stamp duty is also a way to stem the outflow of market funds, foreseeing further improvements in the stock market ecology.

With a reduction in the number of IPOs, declining transaction commissions and stamp taxes, and restrictions on major shareholders reducing their holdings, this year's market reform measures are no less vigorous than the equity reform of 2005. However, while the reforms back then were drastic, the reforms since last year have been more subtle and forward-looking, making the market's future highly promising.