Market Review

Key News

China Market

1. China is expected to raise its deficit ratio from 3% to around 3.8%

To implement the spirit of the meeting of the Standing Committee of the Political Bureau of the CPC Central Committee vigorously, and to ensure funds strongly guarantee the implementation of related work. The Sixth Meeting of the Standing Committee of the 14th National People's Congress voted to pass the resolution of the Standing Committee of the National People's Congress on approving the issuance of additional government bonds by the State Council and the adjustment plan of the central budget for 2023. The central finance will issue an additional 1 trillion yuan of government bonds in the fourth quarter of 2023, as special government bonds management. The national fiscal deficit will increase from 3.88 trillion yuan to 4.88 trillion yuan, with the expected deficit ratio raised from 3% to about 3.8%.

2. Release of China's General Public Budget Revenue and Expenditure for the First Three Quarters

From January to September, the cumulative national general public budget revenue was 16.6713 trillion yuan, up 8.9% year over year. Among this, tax revenue was 13.9105 trillion yuan, up 11.9% year over year; non-tax revenue was 2.7608 trillion yuan, down 4.1% year over year. Looking at the central and local levels, the central general public budget revenue was 7.5886 trillion yuan, up 8.5% year over year; local general public budget primary revenue was 9.0827 trillion yuan, up 9.1% year over year, as shown in the following figure.

Overseas Market

1. The Israeli Military Postpones Attack Due to "Strategic Considerations"

The Times of Israel reports, citing sources, that Israel Defense Forces Chief of Staff Herzl Halevi acknowledged in recent news reports from Gaza that the ground offensive has been postponed for "strategic considerations." Halevi stated that the Israeli paratrooper brigade and the Southern Command have developed high-quality offensive plans to achieve their goals, and the paratrooper brigade has been prepared for drills.

2. S&P Downgrades Israel's Rating Outlook to "Negative"

S&P Global Ratings, one of the three major international rating agencies, has downgraded Israel's sovereign debt outlook from "stable" to "negative," citing the potential for the Israel-Hamas conflict to become more widespread and have a more significant impact on Israel's economy than anticipated. S&P noted that the conflict with Hamas could become more widespread or have a more significant negative impact on Israel's credit metrics than initially expected. Currently, the conflict is expected to remain concentrated in Gaza, with a duration not exceeding three to six months.

3. Escalation of Strikes in the US Automotive Industry

In recent days, the United Auto Workers union has been ramping up pressure on the big three US automakers, with the latest strike action targeting General Motors. About 5,000 workers at General Motors' assembly plant in Arlington, Texas, have joined the strike, one of GM's largest and most profitable factories, producing some of the company's most profitable models, including the Chevrolet Tahoe, GMC Yukon, and Cadillac Escalade large SUVs. The latest strike by 5,000 workers brings the total number of strikers in the major strike action against the three major US automakers that began in September to about 45,000.

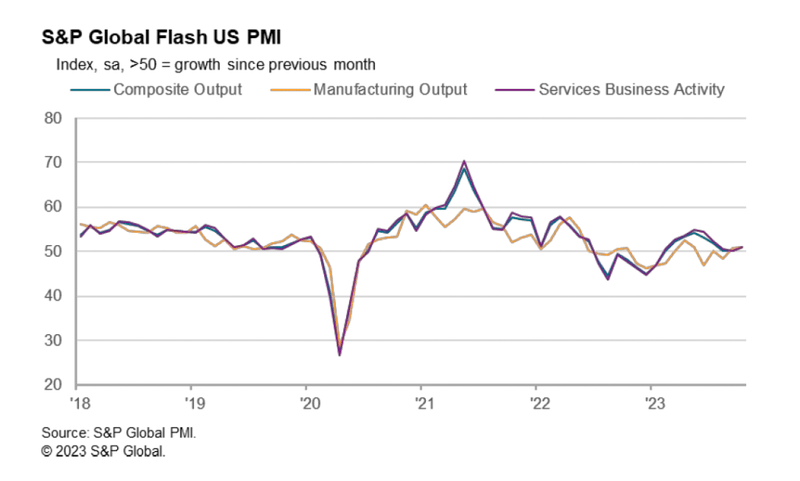

4. US October PMI Surprisingly Exceeds Expectations

Following a stagnation of output in August and September, there was a slight expansion in US manufacturing and service sector activities in October. However, inflationary pressures have weakened, with the pace of cost increases reaching the slowest level in three years. Specifically, the latest data from S&P Global show that the US October Markit Manufacturing PMI initial value reached a six-month high, and the US October Markit Services PMI initial value reached a three-month high, breaking through the economic stagnation indicated by the September PMI readings.

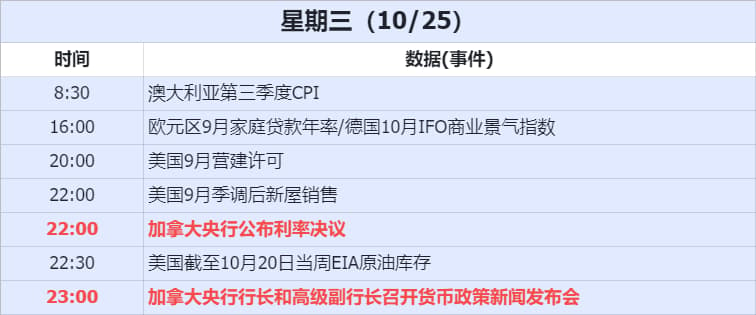

Focus for Today

Today, investors need to pay attention to Australia's Q3 CPI, the German IFO Business Climate Index, US building permits, new home sales, and EIA crude oil inventories, as well as the Canadian interest rate meeting. Besides, investors should also closely monitor the Israel-Palestine situation, and the press conference of the Governor and Senior Deputy Governor of the Bank of Canada among other risk events.