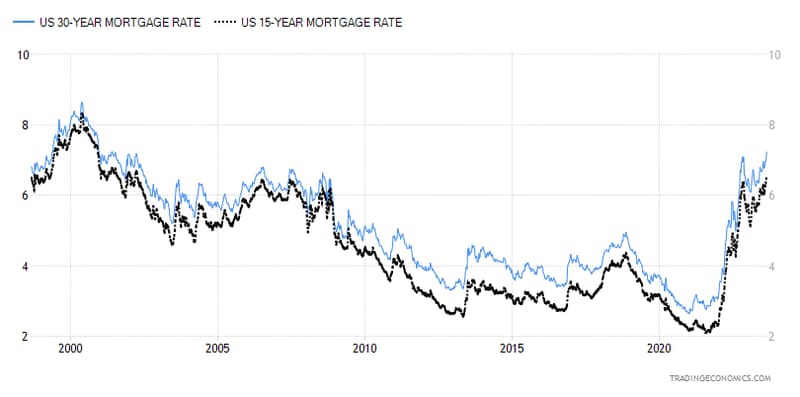

This week, the average long-term mortgage rate in the United States climbed further above 7%, reaching its highest level since 2001, delivering another blow to potential homebuyers struggling to cope with rising house prices and persistently low supply. Data from the mortgage agency Freddie Mac shows that the average rate for a benchmark 30-year home loan jumped from last week's 7.09% to 7.23%, a significant increase from the average rate of 5.55% a year ago.

The average long-term mortgage rate in the United States is now at its highest level since the beginning of June 2001. At that time, the median sale price of a US existing home was $157,500, while the current median sale price of a US existing home has soared to $406,700.

In addition to the average rate for 30-year mortgages reaching its highest level since 2001, data from Freddie Mac shows that the average rate for the 15-year mortgage, a popular choice among homebuyers, rose from last week's 6.46% to 6.55%, compared to an average rate of 4.85% a year ago. Data from the Mortgage Bankers Association (MBA) shows that, as of last week, home loan applications had fallen to their lowest level since 1995, and the median monthly payment listed in home loan applications has been steadily increasing.

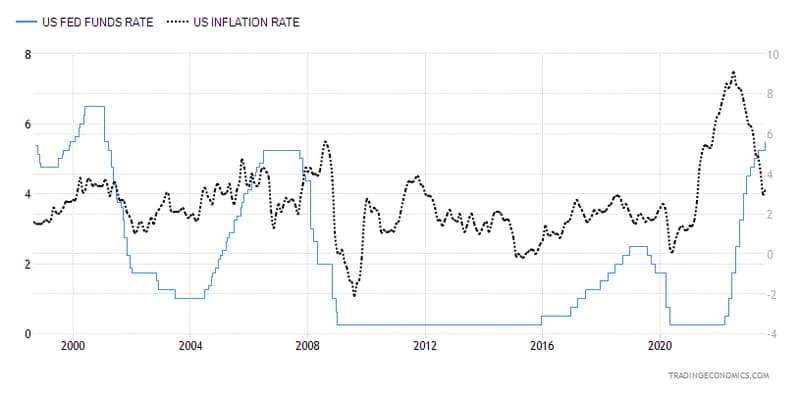

Mortgage rates have been rising alongside the 10-year US Treasury yield, which is a benchmark lenders use to gauge mortgage and other loan rates. Recently, strengthening economic data in the US has led financial markets to worry that the Federal Reserve may further raise interest rates or maintain high rates for a longer time, causing yields on US Treasury bonds of all maturities to rise significantly, especially the 10-year Treasury yield, which has reached its highest level since 2007.

Since last year, in an effort to curb inflationary pressures that have reached as high as 9%, the Federal Reserve has undertaken multiple rate hikes, pushing the benchmark interest rate to multi-year highs. However, the current level of inflation is still far from the Federal Reserve's 2% target, firmly remaining above the average range of the past few decades.

Sam Khater, chief economist at Freddie Mac, indicates that although the average 30-year mortgage rate has reached its highest level since 2001, signs of a continuing strong economy may push the rate even higher.

While mortgage rates do not necessarily reflect the extent of Federal Reserve rate hikes or rate hike expectations, they often follow the trends of the 10-year US Treasury yield. Investors' expectations for future inflation, global demand for US Treasuries, and the Federal Reserve's interest rate policies can all impact mortgage rates.

Beyond the rise in mortgage rates increasing the cost of purchasing homes for consumers, a lack of new home supply and low housing inventory levels are another pressure potential homebuyers must face. According to data from Realtor, the number of new home listings in the US in July fell nearly 21% year-over-year, and sales of existing homes in the first seven months fell 22.3% compared to the same period last year.

Edward Seiler, vice president of housing economics at MBA, mentions that besides the continuously rising mortgage rates, insufficient housing supply is also a problem American consumers have to face. The lower supply of new homes and inventory of existing homes has led to a tight housing supply, keeping the US real estate market in a state of demand outstripping supply, which pushes up the prices of new and existing homes and makes it difficult for them to fall.