In November last year, the Central Financial Work Conference was held in Beijing, where the "Financial Powerhouse" strategy was proposed for the first time. This strategy places significant emphasis on the capital market. For instance, it includes directives like "leveraging the pivotal role of the capital market and deepening the implementation of the stock issuance registration system," and "vigorously enhancing the quality of listed companies, cultivating first-class investment banks and investment institutions." The notion of fostering top-tier investment banks was a first in high-level meetings.

To promote technological innovation and build a modern industrial system, capital support is essential. Traditional bank financing methods, which rely on physical collateral, are not suitable for most light-asset and growth-stage technology companies. Internet giants like Tencent and Alibaba, in their early stages of growth, expanded and strengthened through public market financing.

Since last year's Central Political Bureau meeting, which called for an "active capital market," the China Securities Regulatory Commission (CSRC) has mentioned implementing measures from the perspectives of investment, financing, and assets. The goal set in this Financial Work Conference to cultivate top-tier investment banking institutions will profoundly impact the securities industry. For major brokerage firms, key participants in the securities industry, this presents both challenges and opportunities.

China's securities industry, which started in the 1990s, has seen several rounds of evolution and restructuring. With the industry's maturation, the competitive landscape has stabilized, and there have been significant changes in business operations over the past decade. This article, as the opening piece in a series on the securities industry, aims to outline and analyze the business structure and its transformations in the securities sector.

I. Business Breakdown of Securities Firms

Looking at the business structure of securities firms, they can be categorized into brokerage services, investment banking, asset management, proprietary trading, and net interest income. While some firms differentiate between institutional and retail business or wealth management and capital intermediary services, fundamentally, these are variations of the aforementioned five categories.

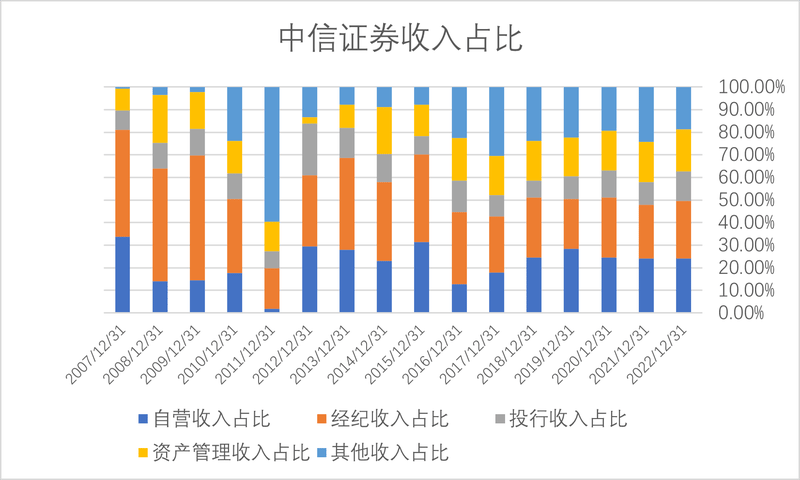

Brokerage services involve earning commissions from investors' buy and sell transactions. Beyond expanding the customer base, commission revenues are largely market-dependent - higher in bull markets and shrinking in bear markets. The industry often likens brokerage services to "earning a living from the weather." For different securities firms, a lower proportion of brokerage business implies a more diversified business structure and stronger risk resistance. For instance, CITIC Securities reported in its 2022 annual report that brokerage income accounted for only 24% of its revenue, significantly lower than its peers.

Investment banking, the second component, includes underwriting fees for IPOs and financial advisory fees for refinancing and mergers and acquisitions. Although not necessarily the most lucrative, investment banking is a core competency for securities firms, heavily reliant on professionalism and resources. Unlike the large workforce in brokerage services, investment banking teams are more streamlined and generate much higher per capita revenue. Firms like Goldman Sachs and Morgan Stanley are globally renowned for investment banking, whereas internet brokers with more extensive brokerage businesses are less well-known to the general public.

The third component is asset management, generally comprising fees and performance rewards from managed client assets, as well as income from stakes in funds or asset management companies. Major securities firms often hold stakes in public fund companies or asset management firms, such as CITIC Securities’ ownership of China Asset Management and GF Securities’ control of GF Fund Management and stake in E Fund Management. In the years 2019 to 2021, the public fund management industry experienced explosive growth in scale and profits, with participating securities firms also benefiting.

However, the accounting of income from publicly traded funds varies among securities firms. If the holding percentage is large enough for consolidation in financial statements (usually over 50%), it’s included under asset management income. Otherwise, it’s counted under investment income.

The fourth business area is proprietary trading, where securities firms invest their own funds. However, their proprietary investments mainly focus on bonds, with riskier derivatives and equity positions primarily used for market-making in over-the-counter options.

For example, CITIC Securities reported a net investment income of CNY 31.69 billion in 2022, plus an unrealized loss of CNY 13.6 billion, leading to a net income of CNY 18.3 billion, accounting for 28% of the revenue. Many wonder how profits were so high in a bearish stock market year. There are two reasons: first, the revenue came from fixed-income assets, with over 88% of the proprietary securities portfolio in fixed income; second, the rapidly growing over-the-counter options business, whose income also falls under proprietary trading. In recent years, investment income has been a major revenue and profit source, consistently generating over CNY 10 billion annually.

The fifth business area is net interest income, generally from the interest differential in securities lending and stock pledge, plus margin interest. This income correlates directly with the scale of brokerage business. Simply put, the larger the brokerage income, the greater the margin interest and securities lending interest, as both are contributed by brokerage clients.

II. Changes Compared to a Past Decade

As the securities industry has matured, there have been significant changes in the revenue structure of brokerage firms. Firstly, there is a diversification in business structure. A decade ago, brokerage firms primarily relied on brokerage services, heavily dependent on market trends for revenue. Although market trends still play a significant role, the scope of services has expanded. With the development of wealth management, margin financing, and derivatives businesses, revenue structures have become more diversified. For instance, CITIC Securities in 2022 reported that proprietary trading, brokerage, investment banking, asset management, and other incomes accounted for 24%, 25%, 13%, 18.7%, and 18.75% of their operating revenue, respectively. This is a significant shift from 2009, when brokerage income comprised 55% of the total, down to 25% last year.

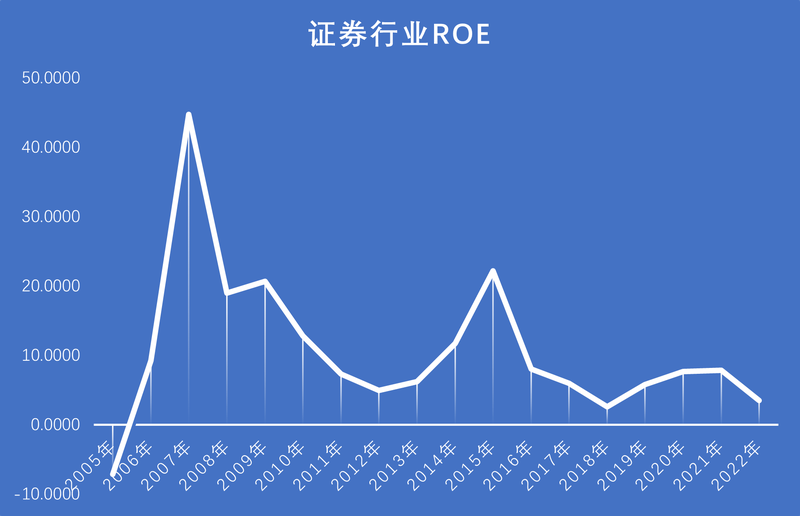

Secondly, the securities industry has moved past its high-growth phase and entered a mature stage. This shift is evident when looking at the industry's net asset return rate. The peak of the return rate was reached in 2015, with fluctuations between 8% to 10% in the last three years. As the industry's assets grow, profit fluctuations are becoming smaller, and stock price elasticity is declining. In the bull market of 2015, the industry saw overall gains of 2 to 3 times, but in the bull market since 2019, the increase has only been about 1 times.

Looking forward, since the wave of innovative businesses that began in 2013, the securities industry has experienced a decade of prosperity and growth. However, the peak of this growth has passed, and business innovation has become more cautious. In recent years, apart from a very cautious approach to on-exchange and off-exchange derivatives, there has been little other innovation. With stock market trading volumes consistently around 1 trillion, the industry's earnings have hit a ceiling, necessitating mergers and reorganizations within the sector to grow stronger and larger.